Ashley O'Malley + Associates have the knowledge, drive, and creativity to help you achieve your real estate goals. They listen carefully to each client and seek to understand their clients' unique style. They work tirelessly to ensure the best possible outcome for every

one of their clients.

Total Sales to Date

Transactions to Date

The East Bay Area is one of the most desirable real estate markets in the world, and we understand that navigating the property buying process can seem challenging. However, with the expertise and breadth of knowledge of Ashley O'Malley + Associates, you are in trusted hands. We will guide and advise you during every step of the buying process to help you find the perfect home that fits your needs, budget, and lifestyle.

1. What is your price range?

2. What type of property are you looking for?

(single-family home, condo, TIC)

3. Do you have any preferred neighborhoods?

4. Do you have pets?

5. Do you have children?

6. Is school proximity an important factor for you?

7. Is proximity to public transportation an important factor?

8. What amenities are most important to you? (parking, yard, etc.)

Reach out Ashley O'Malley + Associates, licensed real estate professionals. We will work as your advocates and trusted advisors to help guide your search.

Before beginning your search, your first step is to get pre-approved for a mortgage loan (unless you will be paying in cash for the full price of your home). We can connect you to a mortgage advisor. Based on your income and credit history, the mortgage advisor will determine how much a bank will lend you, which will help you determine the price range for your search.

Attend viewings and open houses spanning a range of areas and property types. Now is the time to consider your ideal location and amenities.

Reach an agreement with the seller on price and terms. Once you have seen a home you like, you can place an offer, which is a non-binding agreement to pay a certain price for the home. If your offer is lower than the list price, the seller will likely return with a "counter offer", which you can choose to accept, reject, or counter. Our team will advise on pricing throughout the process.

We as your agent will analyze the contract of sale, disclosures and other documents with you. Our job is vital to protecting your interests and understanding the disclosure package.

Work to submit your final offer which includes contract and disclosure package.

Once price is agreed upon, the seller accepts your offer. You then deposit 3% of the purchase price into escrow. This is refundable until all contingencies have beem removed. You are now one step closer to becoming a homeowner!

A final walk-through ensures that the property's condition hasn't changed since your last visit and that the terms of your contract will be met.

Congratulations, you are now a home owner!

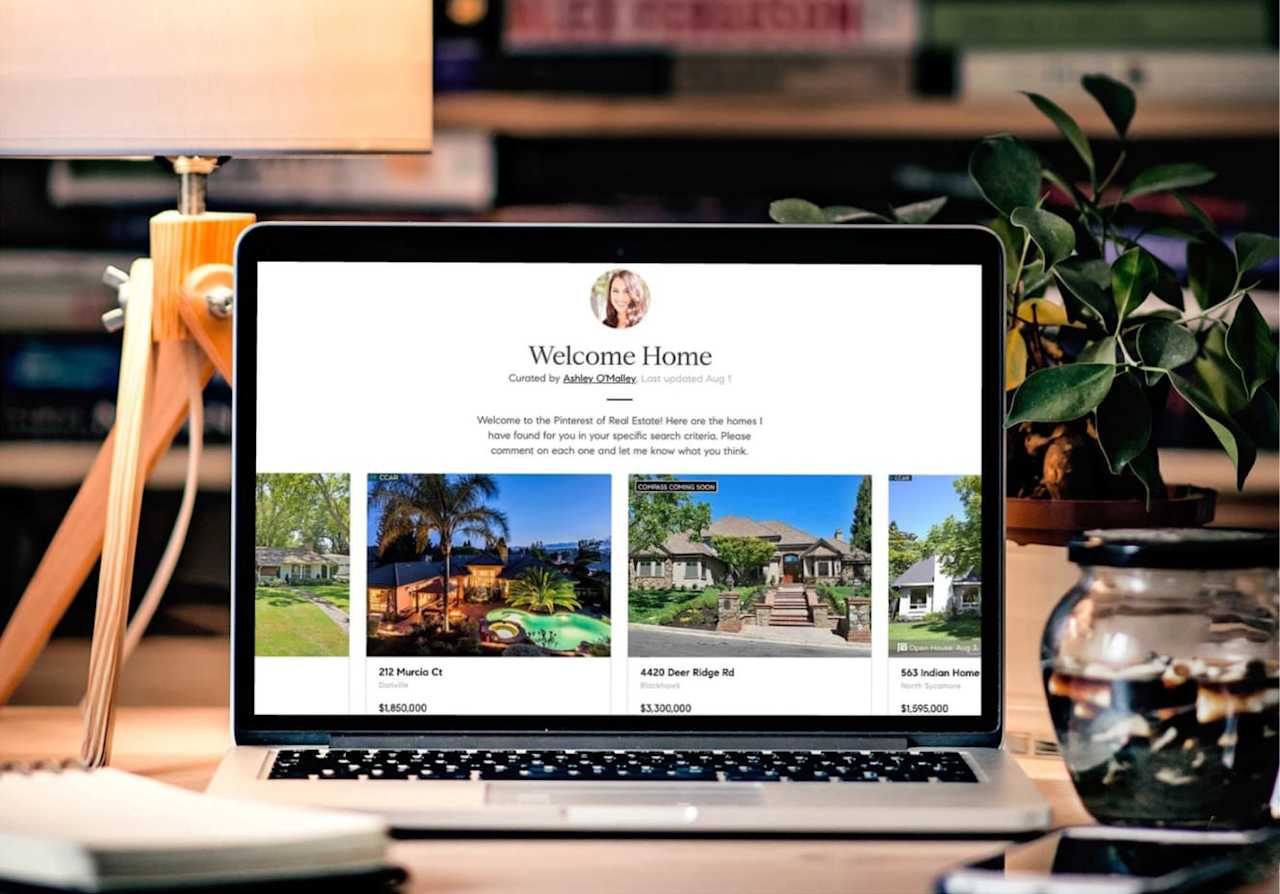

Your own visual portfolio of homes, this platform allows you, you ragent, and anyone else involved in the search to share and track listings. Comment in real time and receive automatic pricing and status updates - all in one, centralized place.

An exclusive first look! Be the first to see new homes with Compass Coming Soon, which offers you a glimpse of select listings before they officially come on the market.

Compass Cares empowers agents to support meaningful causes right where it counts most - in your neighborhood.

Of transactions contribute to a donation in your community.

Donated to strengthen our communities to date.

Organizations supported

Ready to Bring You More Listings...

Sales volume in 2021.

Number of agents.

Amazing Partners: Alain Pinel Realtors, Pacific Union, Paragon

The lender will determine your purchasing power, which gives you a guideline as to what you can afford before you begin the process. They will show you a variety of different types of financing (fixed, adjustable, etc.), and will determine how much you qualify for with each type. Based on your desired payment level and type of financing with which you feel comfortable, we can determine your purchasing power.

You need to choose a home based on what funds you have available; the lender will design a loan that will work for your Individual situation.

Before picking a price range, you should make sure you are comfortable with your total monthly payment: Principle, Taxes, Interest, Insurance (and Mortgage Insurance, if necessary).

In today's market, buyers are not the only parties concerned about financing. Sellers are equally concerned. In cases where there are multiple offers for homes, the buyers must put themselves in the best possible position to have their offers accepted. Getting pre-approved also puts the buyer into a better negotiating position, as the Seller knows the buyer is ready, willing and able to buy, and that financing is not in question. Buyers who are not pre- approved have less chance of obtaining an accepted offer on the house they wish to buy. The buyers must put themselves in the best possible position to have their offer accepted.

Don't forget to ask your lender about closing cost on top of your down payment amount. Some lenders offer closing cost credits. Always worth asking for. If you do not already have a lender, we can refer one to you.

Lenders look carefully at your debt-to-income ratio. A large payment such as a car lease or purchase can greatly impact those ratios and prevent you from qualifying for a home loan.

These transfers show up as new deposits and complicate the application process, as you must then disclose and document the source of funds for each new account. The lender can verify each account as it currently exists. You can consolidate your accounts later if you need to.

A new job may involve a probation period, which must be satisfied before income from the new job can be considered for qualifying purposes.

If the new purchases increase the amount of debt you are responsible for, there is the possibility this may disqualify you from getting the loan, or cut down on the available funds you need to meet the closing costs.

This will show as an inquiry on your lender's credit report. Inquiries must be explained in writing.

before speaking with your lender. The lender can advise you if this needs to be done.

Important paperwork such as W-2 forms, divorce decrees, and tax returns should not be sent with your household goods. Duplicate copies take weeks to obtain, and could stall the closing date on your transaction.

It is important that credit has been established with a good payment history. Any derogatory credit must have a good explanation. Outstanding collection accounts, judgements, or liens must be paid through escrow. The credit report will also list a credit score - a mathematical calculation of your overall credit rating.

A consistent job history with the same company is ideal; however, if changes have been made for advancement, it is acceptable. Schooling completed in preparation for a specific vocation is considered to be a part of your job history.

Your gross monthly income (before taxes) is computed. Bonuses, overtime, part-time, or self-employment income is averaged over the last two years. The principal, interest, taxes, and insurance (PITI) on the new loan (plus mortgage insurance, if applicable) is divided by the gross monthly income to get the "top" ratio. P.I.T.I and all debts are divided by the income to get the "bottom" ratio. Ratios are ideally 33 over 38 for an 80% loan and lower for a 90%, 95% or 97% loan. If other components are strong, higher ratios may be permitted. (PITI / Gross Monthly income = Top Ratio) (Total Debt / Gross Monthly income = Bottom Ratio)

To be considered, your funds must have been verified as having been yours for 3 months. A 5% minimum down payment MUST be from your own funds; however, the remainder of the down payment, closing costs, and the 2 to 3 months of reserves may be gifted by a relative who provides a letter and bank statement showing the ability to give.

The property is the security for the loan. The lender will require an appraisal by a certified fee appraiser to assure that there is sufficient collateral. The underwriter will review the appraisal to verify the marketability, condition, and value of your home. The lender will also review the title report and require title insurance on the property for your protection as well as theirs.

*If you don't fall within these guidelines, don't panic! Lenders work with various investors that offer loan products to fit all situations.

Principle, Interest, Taxes and Insurance

Homeowner's Insurance, Mortgage Insurance, Homeowner's Dues

(Formula for Property Taxes in East Bay Area)

Purchase Price * 1.1782% / 12 Months = Monthly Property Taxes

(Formula for Home Owners Insurance)

Loan Amount * .35% / 12 Months = Monthly Homeowners Insurance

Total monthly payments on installment + revolving debt.

Purchase Price: $1,250,000

Loan Amount: $1,000,000

Down Payment: $250,000

30-yr fixed interest only payment @3.875%

4,702.37 Taxes per month: $1,302.08

HOA Dues (or hazard insurance) $500.00

Total monthly payment (PITI)- $6,504.45

Housing to income ratio 39%

Overall debt service to income raito 41.40%

A single-family home (often abbreviated as SFH), house or dwelling is a free- standing residential building that is maintained as a single dwelling unit. Even if the dwelling unit shares one or more walls with another unit, it is considered a single family home if it has direct access to a street and does not share heating facilities/ equipment, water equipment, nor any other essential facility or service.

A condominium is usually attached housing, where the buyers/owners of each unit own their individual unit and a portion of the private land that the building sits on, as well as any amenities. All condominium buildings have associations (often referred to as Homeowner Associations) that govern/ oversee the policies of the condominium building, allocate expenses for maintenance, and collect the homeowner association fees.

Cooperative (Co-Op) housing is the form of ownership in which the whole property is owned by an cooperation and then sold as shares to the individual buyers/ owners of the community. Cooperative housing typically shares the costs of upkeep and maintenance and shares amenities across all its members.

Tenancy in Common (TIC): In a TIC, a building is owned by a TIC group in percentage shares, including the rights to occupy a unit. Each owner has a distinct, separately transferrable interest in the building as a whole. All areas of the property are owned equally by the group, and therefore an individual may not claim ownership to a specific part of the property.

The escrow period gives all parties involved the time needed to comply with the terms of the offer and prepare to transfer title from the seller to the buyer During this period, you do several things, all of which Ashley O'Malley + Associates will help you with:

You put down a refundable deposit of 3% of the purchase price which is held by the title company.

You have any inspections you wrote into your offer done.

Your lender processes your loan and will ask you for various information needed to approve you.

The lender orders an appraisal for the property.

You review and sign disclosures.

You sign all loans and title documents when they are ready

You do your due diligence on the property, and remove your contigencies by the deadlines you requested in your offer.

Closing happens a couple days after you sign documents

A good offer depends on multiple factors: the market, the neighborhood, the seller needs and the list price. It is our job to provide you with the best information on these factors to help you decide. Is the list price low or high compared to the market? Is your offer the only one or are there several you are up against? Are properties in general selling above or below the asking price in the neighborhood?

Primarily by understanding the strategy and motivation of the sellers. It is important to know how many other offers have been placed, the state of the market, and the goals of the seller. An offer is more than a purchase price - a good offer is drafted carefully with overall terms that will appeal to the seller.

Absolutely. Sellers want to know who is buying their house. Whether you are buying from a developer or individual seller, a solid offer package with a personalized cover letter shows that you are a serious purchaser.

It is preferable to allow 24 hours for the seller to respond. In some cases, the seller requests more time, but usually no more than a couple days.

When you submit an offer, the seller has four choices:

1. They can ACCEPT it as written, and you are ratified meaning you are "in contract" to buy it.

2. They can REJECT it.

3. They can offer you a "BACK-UP position in the case that they have accepted another offer, this will put you in first position to ratify if the first offer cancels or falls through.

4. They can COUNTER your offer. They can counter you on the purchase price, the length of escrow, contingency periods, or any other terms. Once you receive their counter you can then 1) Accept 2) Reject or 3) Counter their counter. This can go back and forth several times until both sides come to an agreement. As soon as one party agrees to the other's counter, you are ratified.

If a seller receives more than one offer, they can counter all of them or a select few. In this scenario, the offer is not ratified when you respond to their counter. The seller has the final say; therefore, you are not ratified until the seller accepts your counter.

Escrow is the period between your offer being accepted and closing escrow. Escrow is a deposit of funds, a deed or other instrument by one party for the delivery to another party upon completion of a particular condition or event.

Whether you are the buyer, seller, lender or borrower, you want assurance that no funds or property will change hands until ALL of the instructions in the transaction have been followed. The escrow holder has the obligation to safeguard the funds and/or documents while they are in the possession of the escrow holder, and to disburse funds and/or convey title only when all provisions of the escrow have been complied with. The escrow officer is a neutral third party and does not represent any one party.

The principals to the escrow-buyer, seller, lender, agents-cause escrow instructions, most usually in writing, to be created, signed and delivered to the escrow officer. If a broker is involved, he will normally provide the escrow officer with the information necessary for the preparation of your escrow instructions and documents. The escrow officer will process the escrow, in accordance with the escrow instructions, and when all conditions required in the escrow can be met or achieved, the escrow will be "closed." The duties of an escrow holder include: following the instructions given by the principals and parties to the transaction in a timely manner; handling the funds and/or documents in accordance with the instruction; paying all bills as authorized; responding to authorized requests from the principals; closing the escrow only when all terms funds in accordance with instructions and provide an accounting for same: the Closing or Settlement Statement. The escrow officer can ONLY take instructions from all parties in agreement. No one party in the transaction can solely give instructions. The escrow officer does not represent any one party-they are a neutral 3rd party in the transaction.

This is determined on a case by case basis and will be written into the offer. Generally, 30 days is common. However, in some cases, you (or the seller) may need more time. In some cases, it is shorter, for example with an all cash deal.

In East Bay Area, it is usually the buyer's choice, as the buyer pays the escrow fees. The selection of the escrow holder is a choice, as the buyer pays the escrow fees. The selection of the escrow holder

is normally done by agreement between the principals. If a real estate broker is involved in the transaction, the broker may recommend an escrow holder. However, it is the right of the principals to use an escrow holder who is competent and who is experienced in handling the type of escrow at hand. There are laws that prohibit the payment of referral fees; this affords the consumer the best possible escrow services without any compromise caused by a person receiving a referral fee.

Real Estate Transfer Disclosure Statement (called the RETDS) and Seller Property Questionnaire

These 2 disclosures are questionnaires about the property completed by the seller

Preliminary Title Report

Provided by the Title Company, this report gives you information about the sellers

Pest Inspection Report

Generally provided by the seller, this report looks specifically at structural damage to the property from wood

boring beetles, termites, dry rot, etc.)

Agent's Visual Inspection Disclosure

It is required that both agents do their own visual inspection

Natural Hazard Zone Disclosure (Property ID or JCP Report)

This report gives you all information about how the property might by affected by a natural hazard. Earthquake, Wildfire, Tsunami, Flood, etc. based on its specific location.

Other Specific County Disclosures

The East Bay Area has many other disclosures that pertain to specific cities and we as your Real Estate team will go over these thoroughly with you prior to signing.

Conditions, covenants and restrictions commonly referred to as CC&Rs

Home Owners Association (HOA) Meeting Minutes for the last 12 months.

HOA Budget and Budget Reserve Study (if it's a larger building)

Condominium Certification Form

House Rules / Misc. Communication

Walk Score

walkscore.com

- Great source for quickly accessing what is nearby.

Crime Mapping

Bay Area Utilities Guide

eastbayrealestatedirectory.com/eastbayutility.html

- This will come in handy when it comes time to turning on your utilities in your new home!

We provide thoughtful and honest counsel which enables clients to make sound, informed decisions. We bring forth powerful negotiation skills and a deep understanding of the housing market in our native Bay Area.